Overview

What is a Collateral Trust?

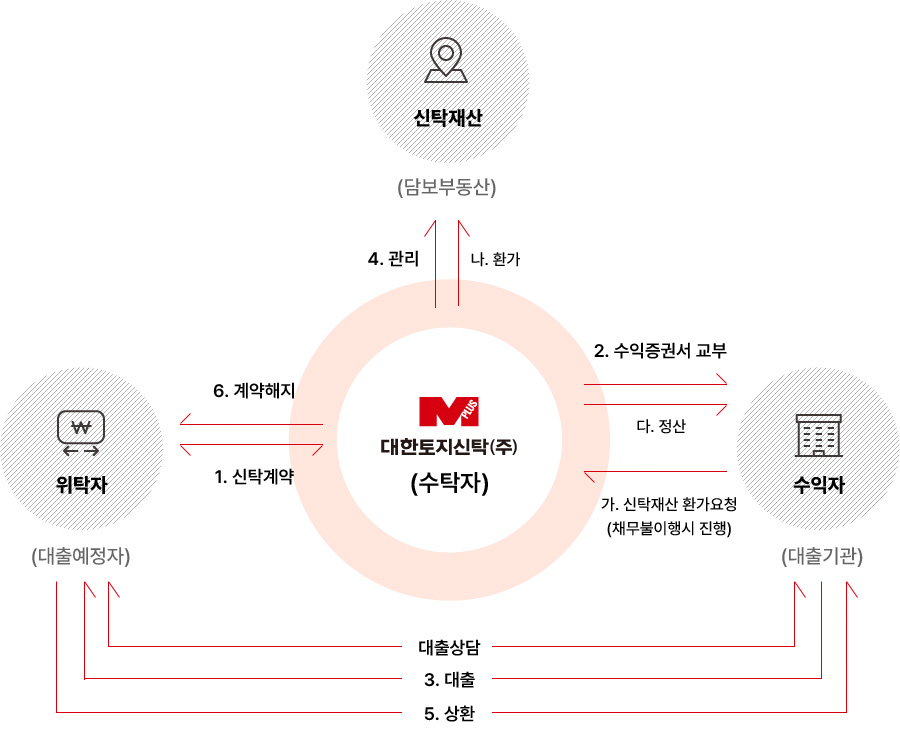

A collateral trust is an advanced financial product that replaces mortgages. It is a product where real estate is entrusted to a trust company, the financial institution is designated as the primary beneficiary, and a beneficiary certificate is issued.

Business Structure

Advantages

An advanced financial product replacing the mortgage system

An advanced financial product replacing the mortgage system

Rapid disposal possible through auction in case of default

Rapid disposal possible through auction in case of default

Minimizes losses by disposing at market-accessible prices

Minimizes losses by disposing at market-accessible prices

Workflow

Click on each step to view more details.

01

Consult and negotiate on loans

- Consult and negotiate loan conditions between lending institution and trustor (debtor)

- Request real estate investigation and analysis from trust company upon loan approval

02

Investigate and analyze collateral real estate (Inspect documents, conduct on-site investigations)

- Investigate rent, tax arrears, senior rights, etc. by the trust company

03

Compile an investigation and analysis report

- Identify real estate status and effective collateral value based on site inspection and rights analysis

- Confirm final trust contract conditions with financial institution

04

Approve loan conditions and request the issuance of a beneficiary certificate

- Record appraisal status, planned loan amount, trust institution, beneficiary certificate amount, etc.

05

Sign a trust contract (Register trust)

- Conclude trust contract between trustor and trust company

- Transfer ownership to trust company (trust registration)

06

Issue and deliver a beneficiary certificate

- Issue beneficiary certificate and copy of trust contract to lending institution

07

Execute a loan

- Send loan execution notice to trust company after loan processing

08

Manage trust property

- Inspect management status on-site upon request of primary beneficiary and notify changes to primary beneficiary

09

Repay the loan

- Return beneficiary certificate to trust company after loan repayment

10

Terminate the trust contract (End the trust)

- Transfer (revert) ownership to trustor by trust company

Realization Procedure (In case of default)

01

Request for realization

- Request realization to trust company when realization factors occur, such as loss of benefit of time

02

Public auction for disposal

- Dispose through open competitive bidding after final demand for debt fulfillment to debtor by trust company

- Can request suspension of realization if necessary

03

Settlement

- Distribute realization proceeds according to the order specified in the trust agreement

- Can request suspension of realization if necessary

Comparison between Collateral Trusts and Mortgages

| Sort | Collateral Trust | Mortgage |

|---|---|---|

| Collateral Setting Method | Transfer of ownership to trust company | Establishment of mortgage right |

| Collateral Real Estate Management | Managed by trust company | Managed by lending institution |

| New Lease, Subordinate Rights Establishment | Can be excluded | Cannot be excluded |

| Occurrence of Priority Claims after Collateral Acquisition | Cannot occur after trust registration | Wage claims can occur |

| Debt Collection Method | Direct auction by trust company | Auction |

| Debt Collection Period | Short-term | Long-term |

| Debt Collection Procedure | Simple | Complex |

| Debt Collection Cost | Low | High |

| Real Estate Disposal Value | Relatively high | Low |

| Exercise of Subrogation Right | No prior seizure necessary | Prior seizure necessary |

| Property Rights Protection | Prevention of third-party rights infringement after trust registration | Third-party seizure possible (Junior mortgage, seizure, provisional attachment of real estate, etc.) |

| Debtor's Cost | Low | High |

| Forced Execution by Junior Right Holders | Selectively possible (with consent of senior right holders) |

It is possible for third-party creditors to apply for compulsory auction or junior mortgage holders to apply for voluntary auction |

| Additional Collateral | Easy to add additional collateral trust (Simple lot addition) |

New establishment contract required |

Problems with the current mortgage system

- Requires excessive time and cost for court auction, which is the method of executing mortgage rights

- Property loss of real estate owners due to low-price successful bids

- Difficulty in managing collateral objects

- Hindrance to the liquidation of real estate value

![]()

Copyright (c) Daehan Real Estate Trust Co.,Ltd All Rights Reserved.